What are guidelines on how to search for e-invoices on the system of tax authority in Vietnam?

What are guidelines on how to search for e-invoices on the system of tax authority in Vietnam?

According to Clause 2, Article 3 of Decree 123/2020/ND-CP, e-invoices are defined as follows:

- An e-invoice is a type of invoice with or without a tax authority code, presented in an e-data format created by an organization or individual selling goods or providing services using e-means, to record sale information according to the provisions of accounting law and tax law. It also includes invoices generated from cash registers connected with e-data transmission to the tax authority. Specifically:

+ An e-invoice with a tax authority code is an e-invoice assigned a code by the tax authority before the organization or individual selling goods or providing services sends it to the buyer.

The tax authority code on the e-invoice includes a transaction number, a unique sequence created by the tax authority's system, and a string of characters encrypted by the tax authority based on the seller's information on the invoice.

+ An e-invoice without a tax authority code is created by the selling organization for goods or services and sent to the buyer without a TIN.

Below is the Guidance on How to Search for E-invoices on the system of tax authority.

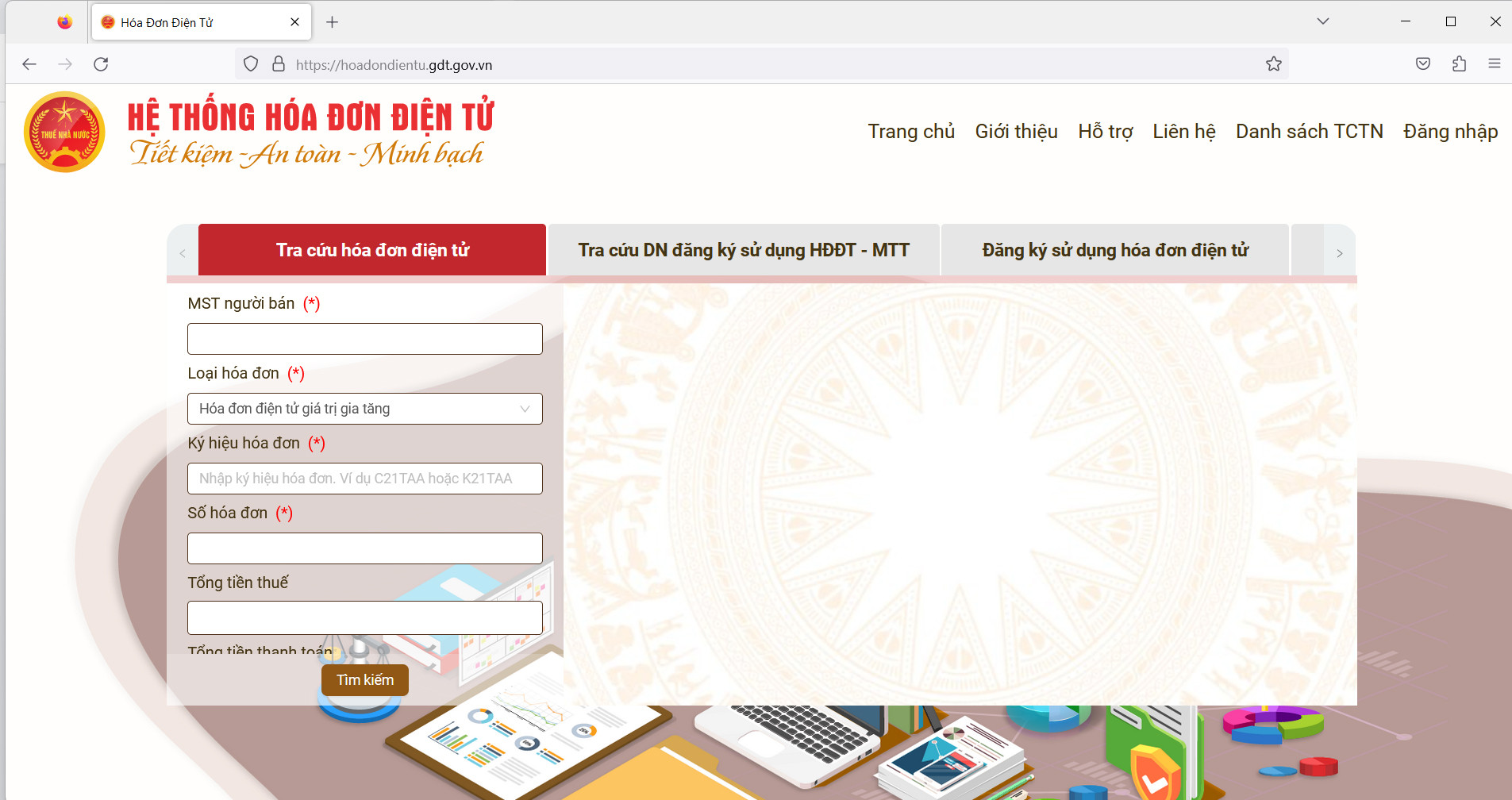

- Step 1: Visit the e-Invoice System website at: https://hoadondientu.gdt.gov.vn/.

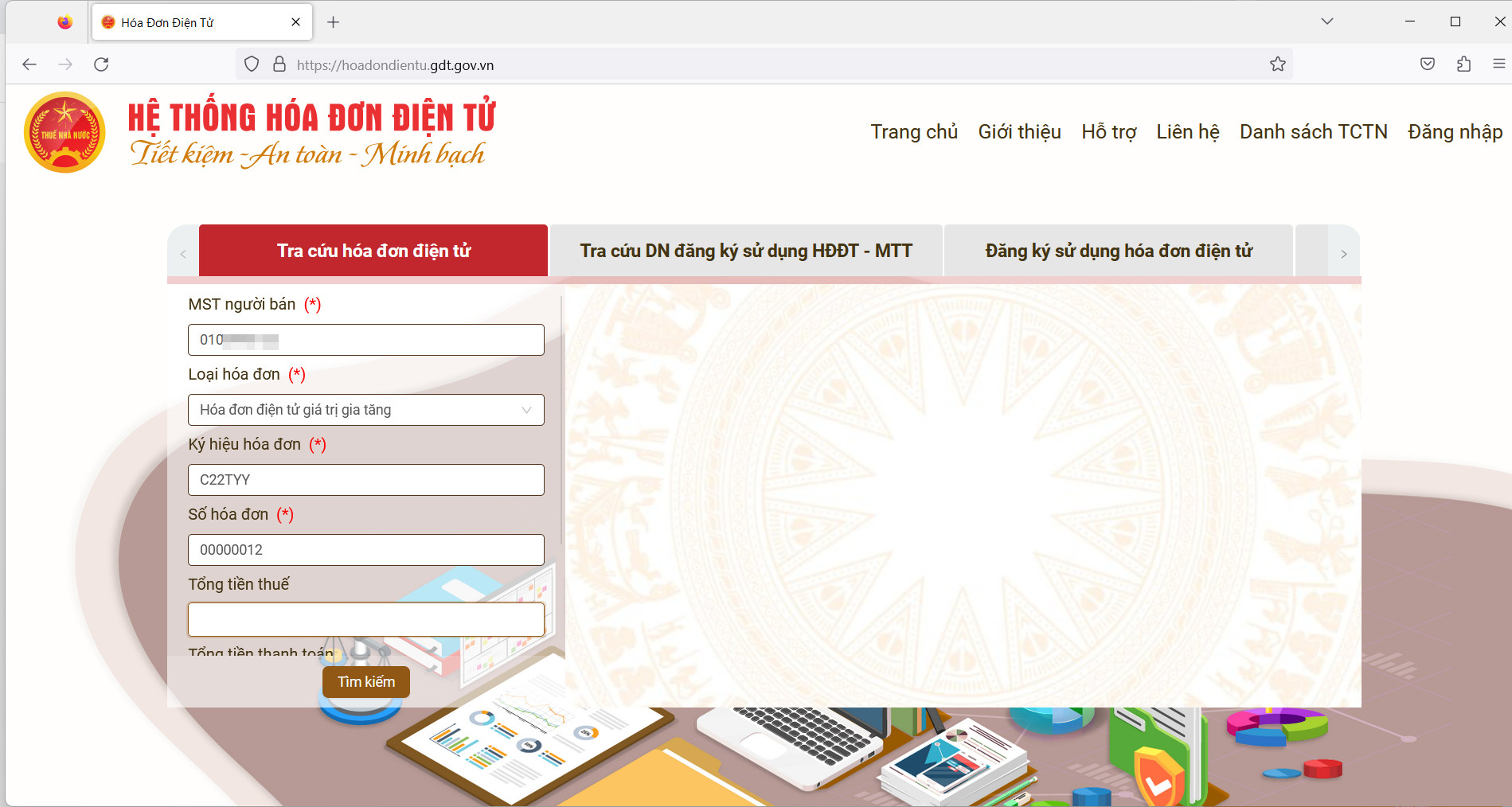

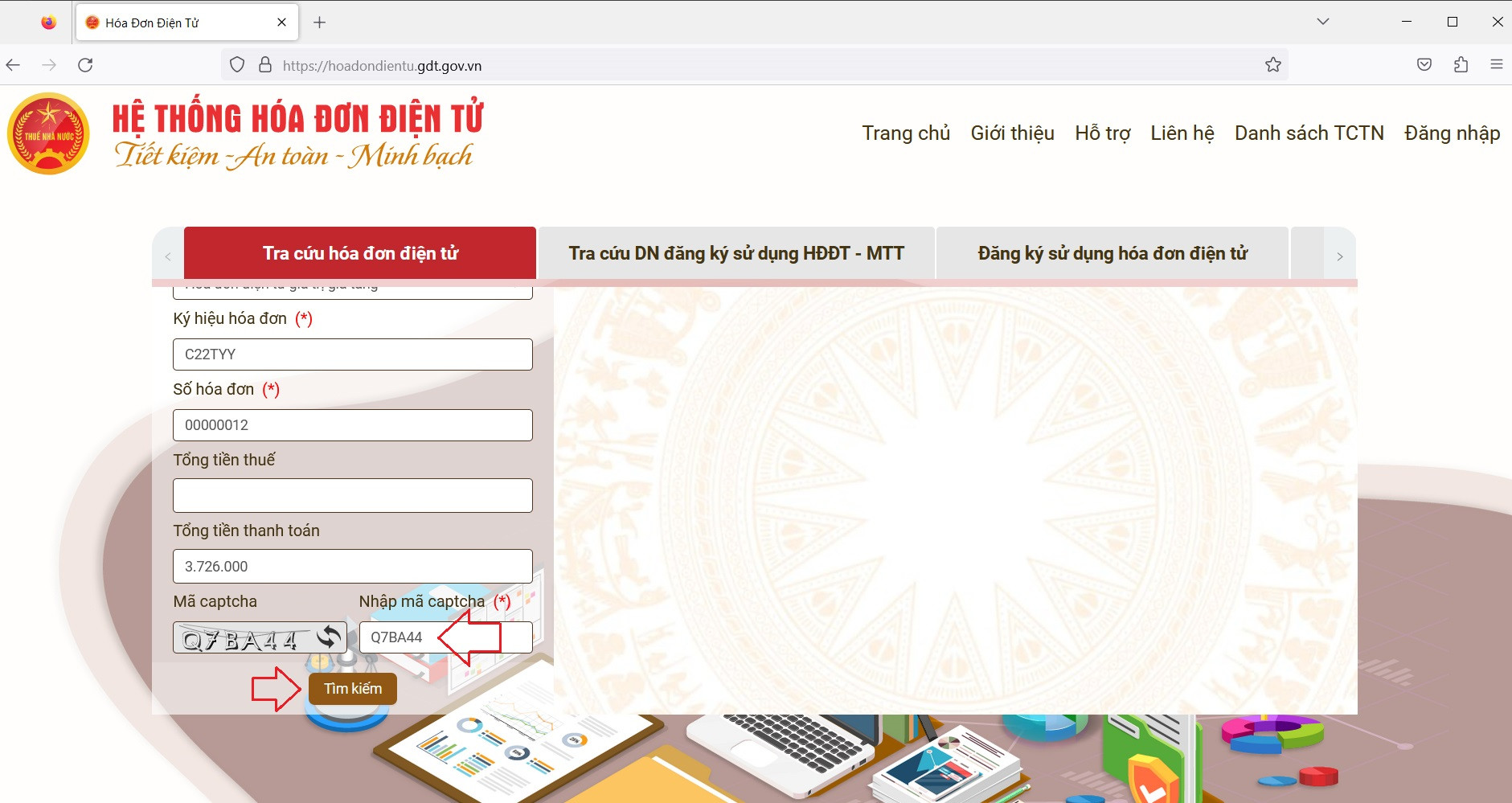

- Step 2: Fully enter the fields marked with a red asterisk (*), including: TIN, invoice type, invoice symbol, invoice number, total tax amount, and total payment amount.

- Step 3: Enter the captcha code and select the "Search" option.

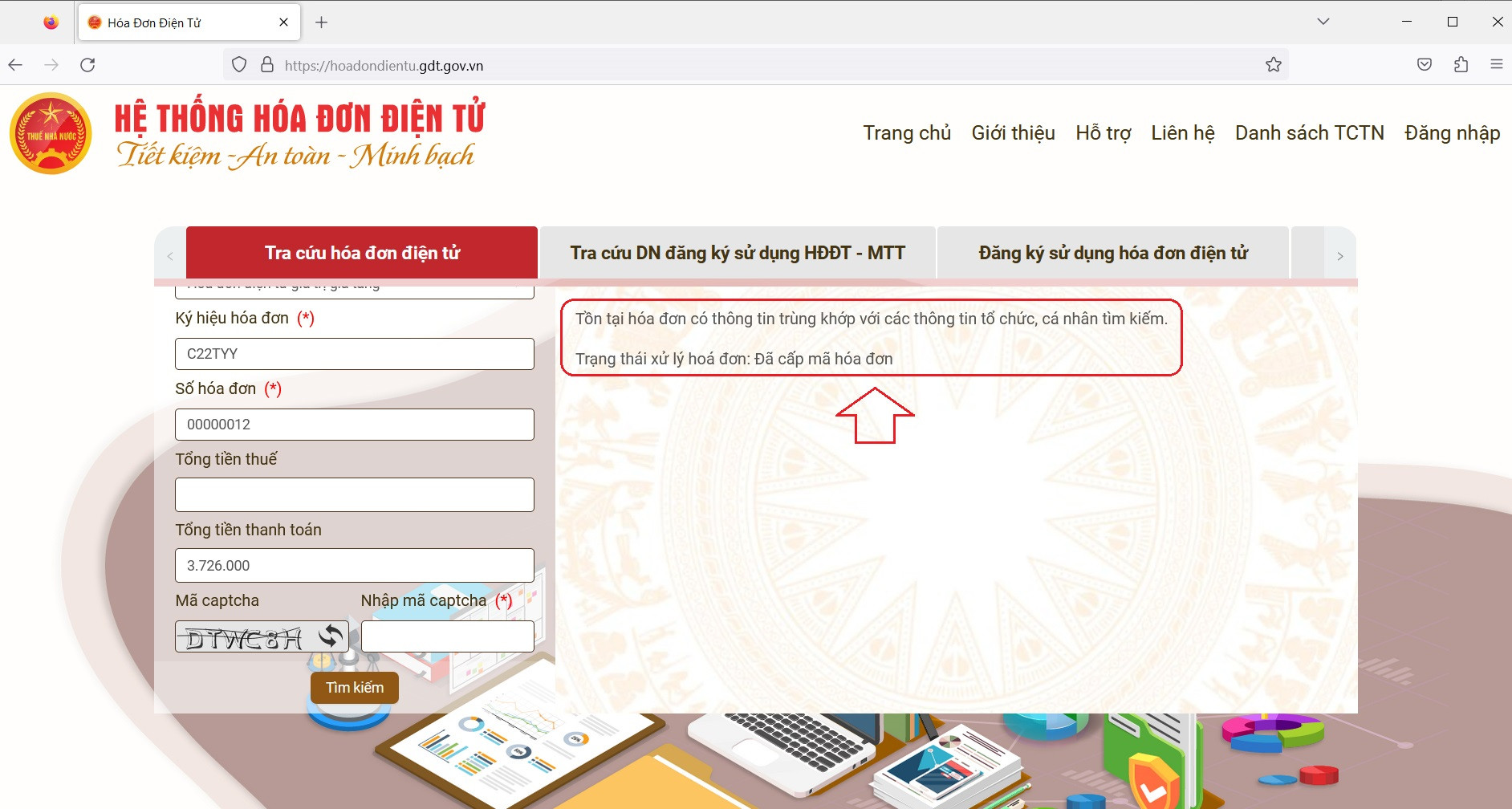

- Step 4: Check the retrieved invoice information results.

A valid invoice will display the invoice processing status as Invoice Code Issued.

In the case of an invalid e-invoice, the system will display "No invoice exists matching the organization's or individual's search information."

To view detailed e-invoices and export them in various formats like Excel, XML, etc., the taxpayer can log into the system of tax authority using the information granted when registering to use e-invoices.

Note*: The content of this Guidance on How to Search for E-invoices on the system of tax authority is for reference purposes only.*

.jpg)

What are guidelines on how to search for e-invoices on the system of tax authority in Vietnam? (Image from the Internet)

What are regulations on the e-invoice format in Vietnam?

According to Article 12 of Decree 123/2020/ND-CP on e-invoice format:

- The e-invoice format is a technical standard stipulating the data type and length of fields serving the transmission, storage, and display of e-invoices. The e-invoice format uses the XML format (XML is the abbreviation of "eXtensible Markup Language" created for sharing e-data between IT systems).

- The e-invoice format consists of two components: the component containing the business data of the e-invoice and the component containing the digital signature data. For e-invoices with a tax authority code, there is an additional component containing data related to the tax authority code.

- The General Department of Taxation develops and publishes the component containing business data of the e-invoice, the component containing the digital signature data, and provides tools to display the contents of the e-invoice under the provisions of Decree 123/2020/ND-CP.

- Organizations and enterprises selling goods, providing services when transmitting e-invoice data to the tax authority directly, must meet the following requirements:

+ Connect to the General Department of Taxation through a private leased line or MPLS VPN Layer 3 channel, consisting of one main channel and one backup channel. Each transmission channel must have a minimum bandwidth of 5 Mbps.

+ Use Web Service or Message Queue (MQ) with encryption as a method to connect.

+ Use the SOAP protocol for packaging and transmitting data.

- e-invoices must display all invoice contents accurately and completely to ensure no misunderstanding by the buyer, readable via e-means.

What are regulations on handling erroneous e-invoices in Vietnam?

According to Article 19 of Decree 123/2020/ND-CP regarding handling erroneous e-invoices:

(1) When the seller discovers that an e-invoice, already coded by the tax authority but not yet sent to the buyer, has errors, the handling is as follows:

The seller notifies the tax authority using Form 04/SS-HDĐT Appendix IA attached to Decree 123/2020/ND-CP regarding canceling an erroneously coded e-invoice and issuing a new e-invoice, digitally signing and sending to the tax authority for a new code to replace the erroneous invoice to send to the buyer. The tax authority will cancel the erroneously coded e-invoice on the system of tax authority.

(2) In cases where e-invoices, whether with or without a tax authority code, have already been sent to the buyer and discovered to have errors, the following handling applies:

- If the error is in the name or address of the buyer but not in the TIN, and other contents are correct, the seller informs the buyer about the erroneous invoice and does not need to issue a new invoice. The seller notifies the tax authority of the error in the e-invoice as per Form 04/SS-HDĐT Appendix IA attached to Decree 123/2020/ND-CP, except in cases where the erroneous e-invoice without a TIN has not been sent to the tax authority.

- If there are errors in: TIN; invoice amount, tax rate, tax amount, or incorrectly specified goods, the seller can choose one of the following options for e-invoice correction:

+ The seller issues an adjusted e-invoice for the erroneous invoice. If the seller and buyer agree to issue an adjustment agreement document before issuing an adjusted invoice, the seller and buyer create and record the errors in the document, and the seller issues the corrected e-invoice.

The corrected e-invoice must contain the phrase "Adjustment for invoice Template number... symbol... number... date... month... year."

+ The seller issues a new e-invoice replacing the erroneous e-invoice unless the seller and buyer agree on creating an adjustment agreement document before issuing the replacement invoice. They create and record the errors so that the seller issues the replacement e-invoice.

The new replacement e-invoice must contain the phrase "Replacement for invoice Template number... symbol... number... date... month... year."

The seller digitally signs the new adjusted or replacement e-invoice and then sends it to the buyer (for e-invoices without a TIN) or submits it to the tax authority to issue a code for the new e-invoice to send to the buyer (for e-invoices with a tax authority code).

- In the aviation industry, corrected invoices for air transport return or exchange documents are considered adjustment invoices without needing information "Adjustment for increased/decreased invoice Template number... symbol... date... month... year." Air transportation companies may issue invoices for refund and exchange cases executed by agents.

(3) If the tax authority detects that an e-invoice, whether with or without a TIN, has errors, it will notify the seller using Form 01/TB-RSDT Appendix IB attached to Decree 123/2020/ND-CP for the seller to check for errors.

Within the notification period specified in Form 01/TB-RSDT Appendix IB, the seller must notify the tax authority using Form 04/SS-HDĐT Appendix IA attached to Decree 123/2020/ND-CP regarding checking the erroneous e-invoice.

After the deadline specified in Form 01/TB-RSDT Appendix IB, if the seller does not notify the tax authority, the tax authority will issue a second notice to the seller using Form 01/TB-RSDT Appendix IB. If there is no response after the second notification period, the tax authority will consider transitioning to a review of e-invoice usage.

(4) Within one working day, the tax authority will notify about the reception and results of processing using Form 01/TB-HDSS Appendix IB attached to Decree 123/2020/ND-CP. Canceled e-invoices are invalid for use but are still stored for reference purposes.