What are cases where employees with income from multiple sources shall declare tax directly in Vietnam?

What are cases where employees with income from multiple sources shall declare tax directly in Vietnam?

Based on the provisions specified at sections d.2 and d.3, point d, clause 6, Article 8 of Decree 126/2020/ND-CP by the Government of Vietnam, employees not under authorization for PIT finalization must directly finalize their personal income tax (PIT).

Types of taxes declared monthly, quarterly, annually, separately, and tax settlement declarations

...

6. Types of taxes and incomes declared annually and settled at the time of dissolution, bankruptcy, activity termination, contract termination, or reorganization of enterprises. In the case of enterprise type conversion (excluding the equitization of state enterprises) where the converting enterprise inherits all tax obligations of the converted enterprise, tax settlement declarations need not be submitted until a decision regarding the conversion is issued; enterprises will declare settlements at fiscal year-end. To be specific:

...

d) Personal income tax for organizations or individuals paying taxable income from salary or wages; individuals authorizing tax settlement to the income-paying organization or individual; individuals directly finalizing taxes with the tax authority. To be specific:

...

d.2) Resident individuals with income from salary, wages authorizing tax settlement to income-paying organizations or individuals. Specifically:

Individuals with income from salary, wages signed under a labor contract of 3 months or more at one location and are actually working there at the time the income-paying organization or individual completes the tax settlement, even if not working a full 12 months in the year. If the individual is transferred from an old organization to a new one per section d.1 of this clause, they may authorize the new organization for tax settlement.

Individuals with income from salary, wages signed under a labor contract of 3 months or more at one place and are working there when the income-paying organization or individual finalizes taxes, even if not working a full 12 months in the year; and also have irregular income from other places averaging no more than 10 million VND per month annually, from which PIT has been withheld at 10%, if not requesting tax settlement for this portion.

d.3) Resident individuals with income from salary, wages directly submitting PIT finalizations with the tax authority in the following cases:

Having excess tax payable or requesting a refund or offset into the next tax period, excluding cases where: the individual owes additional tax of 50,000 VND or less after annual settlement; the tax owed is less than the prepaid tax, and they do not request a refund or offset; individuals earning from salary,

sighed with a labor contract of 3 months or longer with one unit and having irregular income elsewhere averaging no more than 10 million VND annually, with PIT withheld at a rate of 10% when there’s no request, they aren’t required to finalize taxes on this income; where an employer purchases life insurance (excluding voluntary retirement insurance) or non-compulsory insurance with accumulated premiums, and the employer or insurer has withheld PIT at a rate of 10% corresponding to the insurance premium portion bought or contributed by the employer, then the employee is exempt from PIT finalization on this portion.

Individuals present in Vietnam for less than 183 days in the first calendar year, but 183 days or more within 12 consecutive months from the first arrival in Vietnam.

Foreign individuals ending a work contract in Vietnam who finalize tax with the tax authority before departure. If not having finalized taxes, they must authorize the income-paying organization or other entities to finalize according to individual tax finalization regulations. The income-paying organization or entity authorized must bear responsibility for any additional PIT or refund excess.

Resident individuals, receiving income from salary, wages, and eligible for tax reduction due to natural disasters, fires, accidents, or severe illnesses affecting tax payment capacity, shall not authorize the income-paying organization or individual to finalize taxes but must directly submit finalizations with the tax authority as regulated.

...

According to Official Dispatch 801/TCT-TNCN dated March 2, 2016, from the General Department of Taxation guiding PIT finalization for 2015 and dependent taxpayer code issuance, PIT finalization with income from over two places or more is regulated as follows:

- Income-paying organizations, regardless of whether tax is withheld or not, must file PIT finalization and finalize taxes for individuals who authorize them.

- If organizations do not pay salaries, wages in 2015, they are not required to file individual income tax finalizations.

Thus, PIT finalization for individuals with two sources of income in the year will be as follows:

- The income-paying organization finalizes PIT for employees who authorize it (regardless of tax withholding).

- Individuals who earn from salary, wages under a labor contract of 3 months or more with an income-paying organization, and concurrently have irregular income averaging not more than 10 million VND a month annually and having PIT withheld at 10%:

+ If the individual does not require settlement for the irregular income, they may authorize finalization at the income-paying organization with a labor contract of 3 months or more.

+ If the individual requires settlement for the irregular income, they must directly finalize taxes with the tax authority.

- Individuals earning salary, wages under a contract of 3 months or more at one unit and having additional irregular income not withheld with taxes, are required to self-finalize PIT.

Thus, in cases where employees earn from multiple sources and have a labor contract of 3 months or more with one unit and concurrently have irregular income not yet taxed, they must self-calculate and finalize PIT.

What are cases where employees with income from multiple sources shall declare tax directly in Vietnam? (Image from the Internet)

What is the deadline for individuals declaring tax directly in Vietnam?

Pursuant to Section 5 of Official Dispatch 883/TCT-DNNCN of 2022, the regulation is as follows:

According to points a and b, clause 2, Article 44 of Tax Administration Law No. 38/2019/QH14 by the National Assembly, the deadline for PIT finalization declarations is as follows:

- For income-paying organizations: The deadline for submitting tax finalization declarations is the last day of the third month following the end of the calendar year.

- For individuals directly filing returns: The deadline for PIT finalization is the last day of the fourth month following the end of the calendar year. If the individual incurs a PIT reimbursement but submits the finalization declaration late as per regulation, no penalties will apply for late administrative declarations.

- If the tax filing deadline coincides with a public holiday, it extends to the next working day as per the Civil Code.

VI. DUTY OF TAX AGENCIES IN RECEIVING AND PROCESSING PERSONAL INCOME TAX FINALIZATION DECLARATIONS

- Tax agencies must disseminate, guide, and urge taxpayers to execute tax computations and payments accurately, thereby avoiding legal penalties.

- To promote the use of electronic tax filing services (as per the guidance in Official Dispatch No. 535/TCT-DNNCN dated March 3, 2021, by the General Department of Taxation) and e-tax payments on mobile devices (following the guidelines in Official Dispatch No. 4899/TCT-CNTT dated December 14, 2021, by the General Department of Taxation on the deployment of the eTax Mobile 1.0 application), the General Department of Taxation suggests that Tax Departments/Sub-Departments enhance the digital account provision to individuals to facilitate tax computation, simultaneously promoting awareness of the benefits of using tax e-accounts issued by tax authorities such as: individuals computing and paying taxes via electronic means (through the website https://canhan.gdt.gov.vn, or the “Tax e-application” on smart devices) will find the tax computation and submission process more convenient, faster, more efficient without having to submit tax finalization paperwork to tax authorities.

- Tax agencies guide individuals to pay taxes electronically using the electronic tax application on mobile devices as instructed in Appendix II on tax e-payment procedures attached from Official Dispatch No. 4899/TCT-CNTT dated December 14, 2021, by the General Department of Taxation.

- Tax agencies facilitate receiving personal PIT finalization declarations by ensuring convenient processing locations, personnel, and processing times to comply with legal deadlines.

- Tax agencies, after accepting personal PIT finalization declarations, should audit and handle unprocessed applications in the fiscal IT system but proceed per regulations, without returning paperwork unless the individual requests adjustments.

The above are guidelines from the General Department of Taxation regarding some contents on PIT finalizations following current tax legislation. Should any issues arise during implementation, they are to be reported to the General Department of Taxation for prompt guidance./.

Thus, for individuals directly filing taxes, the deadline for submitting PIT finalizations is the last day of the fourth month following the end of the calendar year. For instance, the deadline for PIT finalization for December 2024 is April 30, 2025.

*Note: If individuals have PIT returns to process but submit finalization declarations late, no penalties apply for late tax declaration filings.

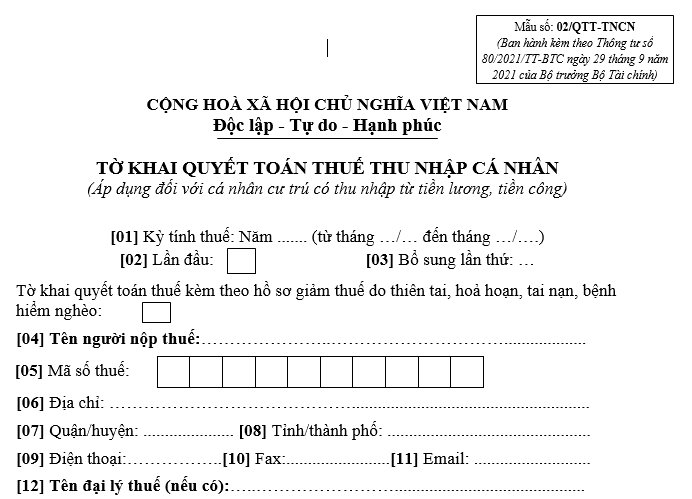

What is the PIT finalization declaration form in Vietnam according to Circular 80?

The PIT finalization declaration form applicable to individuals with income from salaries and wages is form 02/QTT-TNCN issued with Circular 80/2021/TT-BTC, detailed as follows:

>>> Download PIT finalization declaration form applicable to individuals with income from salary, wages.