What are cases of restoration of the tax identification number of an organization in Vietnam?

What are cases of restoration of the tax identification number of an organization in Vietnam?

Based on Clause 3, Article 39 of the Law on Tax Administration 2019, the principles for terminating the validity of a tax identification number are stipulated as follows:

Termination of tax identification number validity

...

- The principles for terminating the validity of a tax identification number are stipulated as follows:

a) The tax identification number shall not be used in economic transactions from the date the tax authority announces the termination of its validity;

b) The tax identification number of an organization, once terminated, shall not be reused, except for cases specified in Article 40 of this Law;

c) The tax identification number of business households or individual business persons, when terminated, shall not affect the validity of the tax identification number of the household representative, which can be used to fulfill other tax obligations of that individual;

...

Once the tax identification number of an organization is terminated, it shall not be reused. However, it can be reused if it falls under the cases stipulated in Article 40 of the Law on Tax Administration 2019 regarding the restoration of tax identification numbers, specifically in the following cases:

- Taxpayers registering concurrently with business registration, cooperative registration, or business operation registration, if the legal status is restored according to the law on business registration, cooperative registration, or business operation registration, shall simultaneously have their tax identification numbers restored.

- Taxpayers who directly register with the tax authority can submit an application for restoring the tax identification number to the directly managing tax authority in the following cases:

+ The competent authority issues a written annulment of the document revoking the business registration certificate or equivalent license;

+ If there is a demand to continue business operations after submitting a termination application but the tax authority has not yet issued a termination notice;

+ When the tax authority issues a notice that the taxpayer is not operating at the registered address but the business registration certificate has not been revoked, and the tax identification number has not yet been terminated.

- The tax identification number can continue to be used in economic transactions from the date the decision restoring the legal status of the business registration authority becomes effective or the date the tax authority announces the restoration of the tax identification number.

What are cases of restoration of the tax identification number of an organization in Vietnam? (Image from the Internet)

What are cases of restoration of the tax identification number of an organization in Vietnam? (Image from the Internet)

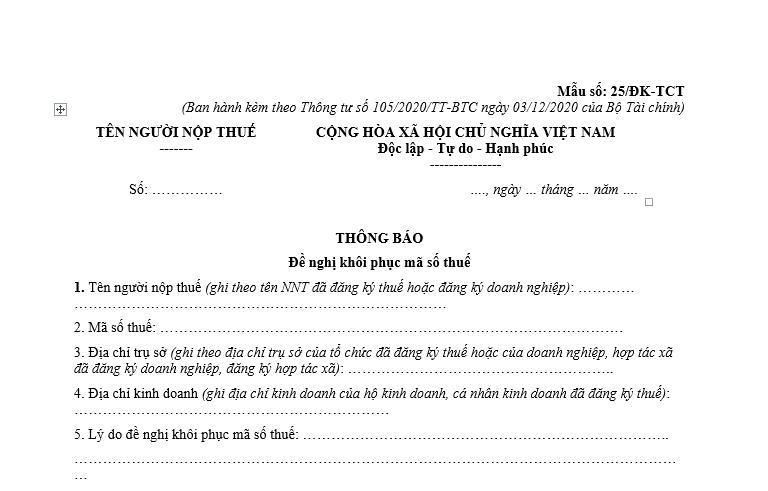

What contents are included in the Form 25/DK-TCT - Application for restoration of a tax identification number in Vietnam?

The current application for restoration of a tax identification number in Vietnam is form 25/DK-TCT, issued together with Circular 105/2020/TT-BTC.

Download the application form for restoration of a tax identification number in Vietnam here

What documents are included in the application for restoration of a tax identification number in Vietnam?

According to Clause 1, Article 18 of Circular 105/2020/TT-BTC, the application for restoration of a tax identification numbers of taxpayers in Vietnam includes:

- Taxpayers as specified in Clause 2, Article 4 of Circular 105/2020/TT-BTC whose Establishment and Operation License or Business Registration Certificate has been revoked by the competent authority and whose tax identification number has been terminated accordingly, but later the competent authority issues a written annulment of the revocation document, must submit an application for restoring the tax identification number to the directly managing tax authority no later than 10 (ten) working days from the date the competent authority issues the annulment document.

The dossier includes:

- Application for restoring the tax identification number using form 25/DK-TCT issued together with Circular 105/2020/TT-BTC;

- A copy of the annulment document issued by the competent authority revoking the Establishment and Operation License or equivalent license.

-

After the tax authority issues a notice regarding the taxpayer not operating at the registered address according to Article 17 of Circular 105/2020/TT-BTC, but the Business Registration Certificate, Cooperative Registration Certificate, Branch/Representative Office Operation Certificate, Business Household Registration Certificate, Establishment and Operation License, or equivalent license has not been revoked and the tax identification number has not yet been terminated, the taxpayer must submit the Application for Restoring a Tax Identification Number form 25/DK-TCT issued together with Circular 105/2020/TT-BTC to the directly managing tax authority before the tax authority issues a notice terminating the tax identification number according to regulations.

-

Taxpayers as specified in Clause 2, Article 4 of Circular 105/2020/TT-BTC who wish to continue business operations after submitting a termination application to the tax authority but the tax authority has not yet issued a termination notice, as regulated in Articles 14 and 16 of Circular 105/2020/TT-BTC, must submit the Application for Restoring a Tax Identification Number using form 25/DK-TCT issued together with Circular 105/2020/TT-BTC to the directly managing tax authority before the tax authority issues a notice terminating the tax identification number.

-

Taxpayers who have submitted a tax identification number termination application due to division, merger, or consolidation according to Article 14 of Circular 105/2020/TT-BTC but later obtain a document annulling the Division Decision, Merger Contract, or Consolidation Contract and the business registration authority or cooperative registration authority has not terminated the operation of the divided, merged, or consolidated enterprise or cooperative must submit the application for restoring the tax identification number to the directly managing tax authority before the tax authority issues a notice terminating the tax identification number according to Article 16 of Circular 105/2020/TT-BTC.

The dossier includes:

- Application for restoring the tax identification number using form 25/DK-TCT issued together with Circular 105/2020/TT-BTC;

- A copy of the document annulling the Division Decision, Merger Contract, or Consolidation Contract.