Vietnam: What is the VAT declaration form for December 2024?

Vietnam: What is the VAT declaration form for December 2024?

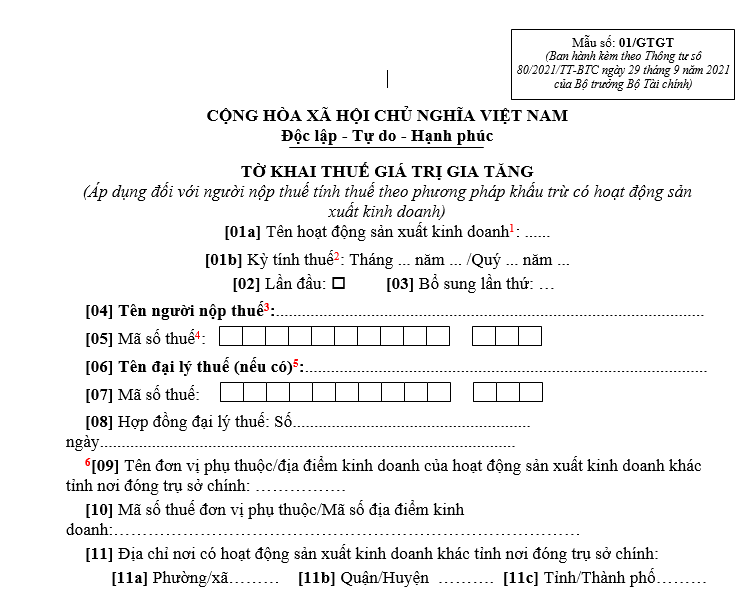

Based on the regulations in Appendix 2 issued with Circular 80/2021/TT-BTC, the VAT declaration form is prescribed as follows:

VAT Declaration Form for December 2024 ....download

Note: The VAT Declaration Form No. 01/GTGT according to Circular 80/2021/TT-BTC is the Value-Added Tax Declaration (applicable to taxpayers calculating tax by the deduction method with production and business activities).

What is the penalty for late submission of the VAT declaration dossier for December 2024?

According to the provisions in Article 13 of Decree 125/2020/ND-CP regarding penalties for violations related to the deadline for submitting tax declaration dossiers, the following apply:

- Warning for submitting the tax declaration dossier 1 to 5 days late with mitigating circumstances.

- A fine ranging from VND 2,000,000 to VND 5,000,000 for submitting the tax declaration dossier 1 to 30 days late, except for cases specified in Clause 1 of this Article.

- A fine ranging from VND 5,000,000 to VND 8,000,000 for submitting the tax declaration dossier 31 to 60 days late.

- A fine ranging from VND 8,000,000 to VND 15,000,000 for one of the following acts:

- Submitting the tax declaration dossier 61 to 90 days late;

- Submitting the tax declaration dossier over 91 days late but no tax payable arises;

- Failing to submit the tax declaration dossier but no tax payable arises;

- Not submitting appendices as required by tax management regulations for businesses with associated transactions along with corporate income tax settlement dossiers.

- A fine ranging from VND 15,000,000 to VND 25,000,000 for submitting the tax declaration dossier more than 90 days late from the deadline, when tax payable arises and the taxpayer has paid all the tax, late payment amount into the state budget before the tax authority announces the decision to inspect or audit the tax or before the tax authority prepares a report on the late submission of the tax declaration dossier as per Clause 11, Article 143 of the Tax Administration Law.

Note: For the same tax or invoice-related administrative violation, the fine for organizations is double the fine for individuals.

Vietnam: What is the VAT declaration form for December 2024? (Image from Internet)

What are prohibited acts in tax administration in Vietnam?

According to Article 6 of the Tax Administration Law 2019, specific prohibited acts in tax administration are as follows:

- Collusion, conniving, or covering up between taxpayers and tax management officials or tax authorities to transfer pricing or evade taxes.

- Causing trouble or harassment to taxpayers.

- Taking advantage to misappropriate or illegally use tax funds.

- Intentionally not declaring or not declaring taxes fully, promptly, and accurately regarding the tax amount payable.

- Obstructing tax management officials from performing their duties.

- Using another taxpayer's tax identification number to commit legal violations or allowing others to use one's tax identification number not conforming to the law.

- Selling goods, providing services without issuing invoices as prescribed by the law, using illegal invoices and using invoices illegally.

- Altering, misusing, unauthorized accessing, or destroying taxpayer information systems.

How to convert the tax declaration period from monthly to quarterly in Vietnam?

According to sub-section 2, Section 1 of the procedures issued with Decision 1462/QD-BTC, the implementation of changing the period for value-added tax, personal income tax from monthly to quarterly is as follows:

*Note: for reference only

Step 1: Prepare a written request to change the tax period from monthly to quarterly using form 01/DK-TDKTT according to Circular 80/2021/TT-BTC.

Step 2: Submit the dossier directly/by post/online to the directly managing tax authority before January 31 of the year you start declaring tax quarterly.

If after January 31 of the year eligible for quarterly tax declaration and no dossier to change the tax period from monthly to quarterly has been submitted, the taxpayer must continue to declare monthly.

If converting the tax declaration period from monthly to quarterly online, proceed as follows:

Access the webpage thuedientu.gdt.gov.vn and log in with the business account (Tax Code-MANAGER) -> Tax Declaration -> Register Declaration Form -> Click Search -> Select VAT Declaration Form (quarterly declaration) -> Select Register to stop the declaration form -> Then register the declaration form and declare monthly.

Step 3: The tax authority receives the dossier and processes it according to regulations.

The tax authority informs the acceptance or non-acceptance of the dossier no later than one working day from the date indicated on the receipt of the dossier.