Shall an accounting unit whose most revenues and expenditures are in a foreign currency notify the tax authority in Vietnam?

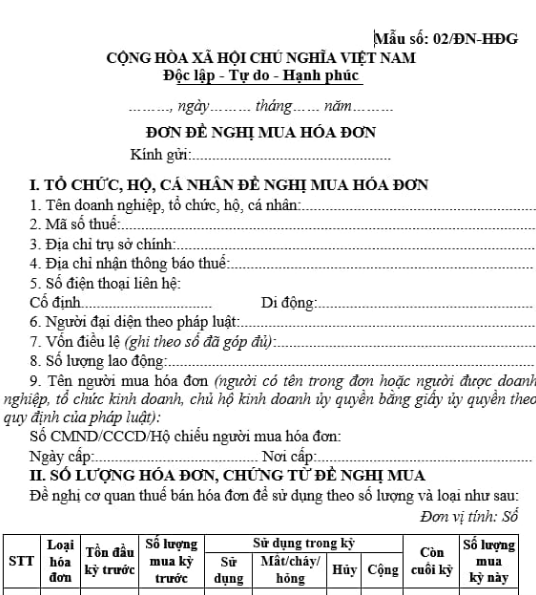

What is the application form to purchase tax authority-ordered printed invoices in Vietnam?

The request form to purchase tax authority-ordered printed invoices is form No. 02/DN-HDG issued along with Decree 123/2020/ND-CP, which stipulates as follows:

Download the latest request form to purchase tax authority-ordered printed invoices.

Shall an accounting unit whose most revenues and expenditures are in a foreign currency notify the tax authority in Vietnam? (Image from the Internet)

Shall an accounting unit whose most revenues and expenditures are in a foreign currency notify the tax authority in Vietnam?

Based on Article 10 of the Law on Accounting 2015 regulating the units of measurement used in accounting as follows:

Units of measurement used in accounting

1. The currency unit used in accounting is the Vietnamese Dong, with the national symbol "đ" and the international symbol "VND". In cases where economic and financial transactions are carried out in foreign currencies, the accounting unit must record them in the original currency and in Vietnamese Dong at the actual exchange rate, unless otherwise provided by law; for foreign currencies without exchange rates against the Vietnamese Dong, they must be converted through a foreign currency with an exchange rate against the Vietnamese Dong.

An accounting unit whose most revenues and expenditures are in a foreign currency can choose that foreign currency as the monetary unit for accounting, responsible before the law and notify the directly managing tax authority. When preparing financial reports used in Vietnam, the accounting unit must convert to the Vietnamese Dong at the actual exchange rate, unless otherwise provided by law.

2. The physical units and labor time units used in accounting are legal measurement units of the Socialist Republic of Vietnam; when an accounting unit uses different measurement units, they must be converted to the legal measurement units of the Socialist Republic of Vietnam.

3. Accounting units are allowed to round numbers and use simplified measurement units when preparing or publicly disclosing financial reports.

4. the Government of Vietnam shall detail and guide the implementation of this Article.

Therefore, according to the above regulation, an accounting unit whose most revenues and expenditures are in a foreign currency must notify the directly managing tax authority.

Does the tax authority have the authority to inspect accounting in Vietnam?

Based on Article 34 of the Law on Accounting 2015 regulating the units of measurement used in accounting as follows:

Accounting inspection

1. An accounting unit must be subjected to accounting inspection by competent authorities. Accounting inspection shall be conducted only upon the decision of a competent authority according to the provisions of law, except for the bodies stipulated at point b clause 3 of this Article.

2. Competent authorities deciding on accounting inspection include:

a) Ministry of Finance;

b) Ministries, ministerial-level agencies, agencies under the Government of Vietnam, and other central agencies, deciding the inspection of accounting units in the fields assigned for management;

c) Provincial People's Committees decide on the inspection of accounting units at the localities under their management;

d) Superior units decide to inspect the accounting units under their management.

3. Competent authorities to conduct accounting inspections include:

a) The authorities stipulated in clause 2 of this Article;

b) State inspectorate, specialized financial inspectors, state audit, tax authorities when conducting inspections, checks, audits on accounting units.

Accordingly, the tax authority has the authority to inspect accounting when conducting inspections, checks, and audits of accounting units.

May tax authority-ordered printed invoices be destroyed by burning?

According to clause 11 of Article 3 Decree 123/2020/ND-CP which provides as follows:

Interpretation of terms

In this Decree, the following terms shall be understood as follows:

...

11. Destruction of invoices, documents:

a) The destruction of electronic invoices and documents is a measure to make the electronic invoices and documents no longer exist on the information system, being inaccessible and not referable to the information contained in such electronic invoices and documents.

b) The destruction of paper tax authority-ordered printed invoices, printed documents, self-printed is to use measures such as burning, cutting, shredding, or other destruction methods ensuring that invoices and documents once destroyed cannot be reused for their information and data.

12. An e-invoice service provider is an organization that provides solutions for the creation, connection, receipt, transmission, processing, and storage of e-invoice data with and without a code from the tax authority. E-invoice service organizations include: Organizations providing e-invoice solutions with and without codes from the tax authority to sellers and buyers; organizations connecting receipt, transmission, storage of e-invoice data with the tax authority.

13. An e-invoice database is a collection of data about e-invoices of organizations, enterprises, and individuals when selling goods and providing services and information about electronic documents of organizations and individuals using them.

Accordingly, the destruction of tax authority-ordered printed invoices is understood as using measures such as burning, cutting, shredding, or other destruction methods to ensure that the destroyed invoices and documents cannot reuse their information and data.

Therefore, it is entirely possible to destroy tax authority-ordered printed invoices by burning them.