Is the tracing of tax payment information considered an e-document in Vietnam?

Is the tracing of tax payment information considered an e-document in Vietnam?

Based on Article 6 of Circular 19/2021/TT-BTC, the regulation on e-documents in e-tax transactions includes the following types:

[1] e-tax dossiers

which include:

- Taxpayer registration dossiers;

- Tax declaration dossiers; confirmation of tax obligations;

- tracing of tax payment information;

- Procedures for offsetting tax, late payment interest, fines for overpayment;

- Tax refund dossiers; tax reduction dossiers; exemption from late payment interest; non-calculation of late payment interest;

- Dossiers for freezing tax debts; dossiers for waiving tax debts, late payment interest, fines; tax deferral; installment tax debt payment and other e-tax documents as stipulated in the Law on Tax Administration and guiding documents of the Law on Tax Administration.

[2] e-state budget payment documents: State budget payment documents as stipulated in Decree 11/2020/ND-CP, in e-form. In case taxes are paid through the e-tax payment form of banks or intermediary payment service providers, the state budget payment document is the transaction document of the bank or intermediary payment service provider, which must ensure all information as per the state budget payment document template.

[3] Notifications, decisions, other documents from tax authorities in e-form.

[4] e-documents pursuant to this provision must be electronically signed as prescribed in Article 7 of Circular 19/2021/TT-BTC.

In cases where e-tax dossiers include documents in paper form, these must be converted to e-form as stipulated by the Law on e-Transactions and Decree 165/2018/ND-CP.

Referring to the regulations, there are fundamentally four types of e-documents among which there are e-tax dossiers that include:

- Taxpayer registration dossiers;

- Tax declaration dossiers; confirmation of fulfilling tax obligations;

- tracing of tax payment information;

- Procedures for offsetting tax, late payment interest, fines for overpayment;

- Tax refund dossiers; tax reduction dossiers; exemption from late payment interest; non-calculation of late payment interest;

- Dossiers for freezing tax debts; dossiers for waiving tax debts, late payment interest, fines; tax deferral;

Thus, considering the above regulation, the tracing of tax payment information is part of the e-tax dossier and is therefore regarded as an e-document.

Is the tracing of tax payment information considered an e-document in Vietnam? (Image from the Internet)

Vietnam: When does an e-document have the have the same validity as physical one?

Based on Clause 2, Article 6 of Circular 19/2021/TT-BTC, it is stipulated as follows:

e-documents in e-tax transactions

...

2. The legal value of e-documents: e-documents as prescribed in this Circular have the same value as paper dossiers, documents, notifications, and other papers. An e-document is valued as an original if carried out by one of the methods prescribed in Article 5 of Decree 165/2018/ND-CP.

Thus, according to the aforementioned regulation, an e-document holds the have the same validity as physical one when implemented by one of the methods described in Article 5 of Decree 165/2018/ND-CP as follows:

Method [1]: The e-document is digitally signed by the agency, organization, or individual initiating the e-document and the agency, organization, or individual related as prescribed by specialized law.

Method [2]: The information system ensures the integrity of the e-document during transmission, receipt, and storage on the system; records agencies, organizations, or individuals that initiated e-documents and those responsible who participated in processing the e-documents and applies one of the following measures for authenticating entities involved in creating and processing e-documents: authentication with a digital certificate, biometric authentication, two-factor authentication including a one-time password or a random authentication code.

Method [3]: Other measures mutually agreed upon by the parties in the transaction, ensuring data integrity, authenticity, non-repudiation, and in accordance with the Law on e-Transactions.

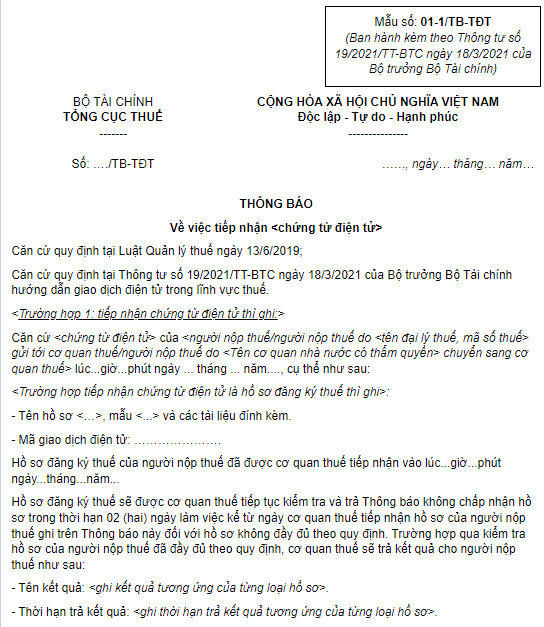

What is the form for notification of receiving e-documents in Vietnam?

Based on the form catalog, the Notification of receiving e-documents is form 01-1/TB-TDT issued with Circular 19/2021/TT-BTC as follows:

Download Form for Notification of Receiving e-Documents.