Is the production of PE plastic bags subject to environmental protection tax?

What is a PE plastic bag?

Pursuant to Article 2 of the 2010 Law on environmental protection tax, a definition is provided for polyethylene (PE) plastic bags falling under the category of environmental protection tax, as follows:

Terminology Explanation

In this Law, the terms below are understood as follows:

1. environmental protection tax is an indirect tax levied on products and goods (hereinafter collectively referred to as goods) that have a negative impact on the environment when used.

2. Absolute tax rate is the tax rate stipulated as an amount calculated on a taxable unit of goods.

3. Plastic bags subject to tax are bags and packaging made from single-layer polyethene film, technically known as air-tight plastic bags.

4. Hydro-chloro-fluoro-carbon (HCFC) solution is a group of ozone-depleting substances used as refrigerants.

As per laws, plastic bags subject to tax are defined as bags and packaging made from single-layer polyethene film, technically known as air-tight plastic bags.

This aligns with the regulation that PE plastic bags are made from polyethylene (PE) resin. PE is a lightweight, flexible plastic that is durable and water-resistant.

Does PE plastic bag production incur environmental protection tax in Vietnam? (Image from Internet)

Is the production of PE plastic bags subject to environmental protection tax?

The entities subject to environmental protection tax are stipulated in Article 3 of the 2010 Law on environmental protection tax as follows:

Taxable Entities

1. Gasoline, oil, lubricant, including:

a) Gasoline, except ethanol;

b) Jet fuel;

c) Diesel oil;

d) Kerosene;

đ) Mazut oil;

e) Lubricating oil;

g) Lubricating grease.

2. Coal, including:

a) Brown coal;

b) Anthracite coal;

c) Fat coal;

d) Other types of coal.

3. Hydro-chloro-fluoro-carbon (HCFC) solution.

4. Plastic bags subject to tax.

...

Additionally, the entities subject to environmental protection tax are guided by Article 2 of Decree 67/2011/ND-CP (amended by Article 1 of Decree 69/2012/ND-CP) as follows:

The taxable entities are implemented according to the provisions of Article 3 of the 2010 Law on environmental protection tax.

- For gasoline, oil, lubricant stipulated in Clause 1 of Article 3 of the 2010 Law on environmental protection tax is fossil fuel-based. For mixed fuels containing biofuel and fossil fuel-based gasoline, oil, and lubricant, only environmental protection tax on the fossil fuel portion is calculated.

- For hydro-chloro-fluoro-carbon (HCFC) solution stipulated in Clause 3 of Article 3 of the 2010 Law on environmental protection tax is the type of gas used as a refrigerant and in the semiconductor industry.

- For plastic bags subject to tax (plastic bags) stipulated in Clause 4 of Article 3 of the 2010 Law on environmental protection tax, these are thin plastic bags, containing mouths, bottoms, sides, and capable of holding products, made from single-layer HDPE (high-density polyethylene resin), LDPE (Low-density polyethylene), or LLDPE (Linear low-density polyethylene resin), except for pre-packaged goods and plastic bags meeting environmental standards regulated by the Ministry of Natural Resources and Environment.

The pre-packaged goods mentioned above (including those shaped as bags and unshaped) include:

+ Pre-packaged goods imported;

+ Packaging produced or imported by organizations, households, or individuals to package products produced, processed, or purchased for packaging or packaging services;

+ Packaging bought directly from manufacturers or importers by organizations, households, or individuals to package products produced, processed, or purchased for packaging or packaging services.

- For herbicides limited in use, termite prevention chemicals, wood preservatives limited in use, fumigants limited in use, stipulated in Clauses 5, 6, 7, and Clause 8 of Article 3 of the 2010 Law on environmental protection tax: Detailed implementation is according to Resolution No. 1269/2011/UBTVQH12 dated July 14, 2011, of the Standing Committee of the National Assembly on the environmental protection tax table.

Therefore, it is clear that enterprises producing PE plastic bags must incur environmental protection tax.

How much environmental protection tax for PE plastic bags in Vietnam?

Based on Article 8 of the 2010 Law on environmental protection tax concerning the tax frame schedule:

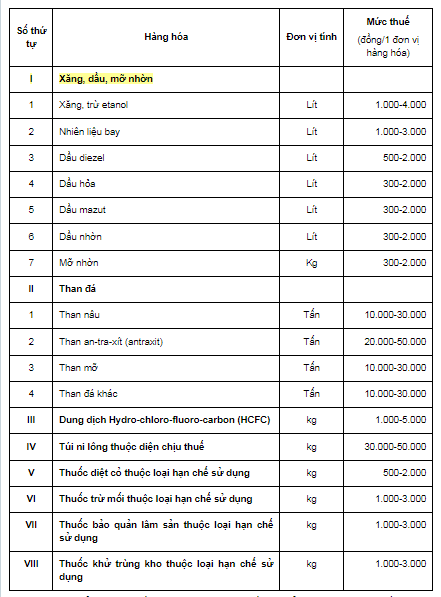

- The absolute tax rate is specified in the Tax Frame below:

- Based on the Tax Frame stipulated in Clause 1 Article 8 of The 2010 Law on environmental protection tax, the Standing Committee of the National Assembly prescribes a specific tax rate for each type of taxable goods ensuring the following principles:

+ The tax rate for taxable goods aligns with the State's economic-social development policy in each period;

+ The tax rate for taxable goods is determined according to the degree of negative impact on the environment caused by the goods.

Therefore, the tax rate that PE plastic bags are subject to is between 30,000 to 50,000 VND per unit of goods, with the unit being calculated in kilograms.