Is inheritance in the form of money and gold subject to personal income tax in Vietnam?

Is inheritance in the form of money and gold subject to personal income tax in Vietnam?

Based on Clauses 1 to 10, Article 3 of the 2007 Law on Personal Income Tax, which lists 10 types of income subject to personal income tax (PIT) as follows:

To be specific: the income types mentioned in Article 3 of the 2007 Law on Personal Income Tax (amended by Clauses 1 and 2 of Article 2 of the 2014 Law on Amendments to Laws on Tax and further amended by Clause 1 of Article 1 of the 2012 Revised Law on Personal Income Tax) as follows:

Taxable Income

Taxable personal income includes the following types of income, except for income exempt from tax as specified in Article 4 of this Law:

1. Income from business, including:

a) Income from production and trading of goods and services;

b) Income from independent professional activities of individuals with licenses or certificates to practice according to the law.

Income from business as specified in this clause does not include income of businesses with annual revenue of 100 million VND or less.

2. Income from wages and salaries, including:

a) Wages, salaries, and other amounts of similar nature;

b) Allowances and subsidies, except for the allowances and subsidies provided by the law on preferential treatment for people with meritorious services; national defense and security allowances; toxic and hazardous allowances for certain sectors or professions at workplaces with toxic and hazardous elements; attraction allowances, regional allowances as provided by law; emergency hardship subsidies, labor accident subsidies, occupational disease subsidies, one-time subsidies for childbirth or adoption, allowances due to reduced labor ability, one-time retirement subsidies, monthly pensions, and other subsidies as per the law on social insurance; severance pay, job loss allowances in accordance with the Labor Code; social protection subsidies, and other allowances and subsidies not of wage and salary nature as prescribed by the Government of Vietnam.

3. Income from capital investment, including:

a) Loan interest income;

b) Dividend income;

c) Income from other forms of capital investment, except for government bond interest income.

4. Income from capital transfer, including:

a) Income from transferring shares in economic organizations;

b) Income from securities transfer;

c) Income from capital transfer under other forms.

5. Income from real estate transfer, including:

a) Income from transferring land use rights and assets attached to land;

b) Income from transferring ownership or use rights of houses;

c) Income from transferring lease rights on land, water surface;

d) Other income received from real estate transfer in any form.

6. Income from winnings, including:

a) Lottery winnings;

b) Winnings from promotional activities;

c) Winnings from betting;

d) Winnings from games, contests, and other forms of winnings.

7. Income from royalties, including:

a) Income from transferring, licensing intellectual property rights;

b) Income from technology transfer.

8. Income from franchising.

9. Income from inheritance is securities, shares in economic organizations, business establishments, real estate, and other assets which must be registered for ownership or use right.

10. Income from gifts is securities, shares in economic organizations, business establishments, real estate, and other assets which must be registered for ownership or use right.

The Government of Vietnam stipulates detailed provisions and guidelines for the implementation of this Article.

Additionally, Article 4 of Decree 65/2013/ND-CP prescribes 14 types of income that are exempt from PIT as follows:

Income Exempt from Tax

1. Income from real estate transfer (including residential houses, future-formed buildings as stipulated by the law on real estate business) between: husband and wife; biological parents and children; adoptive parents and adopted children; parents-in-law and daughter-in-law; parents-in-law and son-in-law; paternal grandparents and grandchildren; maternal grandparents and grandchildren; siblings.

2. Income from transferring a residential house, residential land use rights, and assets attached to residential land of an individual in the case where the transferor owns only one residential house, residential land use right in Vietnam.

An individual transferring only one residential house, residential land use right in Vietnam as mentioned in this Clause must meet the following conditions:

a) At the time of transfer, the individual owns or uses only one residential house or one parcel of land (including cases where there is a house or construction attached to that parcel);

b) The duration of ownership or use rights over the residential house, residential land must be at least 183 days at the time of transfer;

c) The residential house, land use right is fully transferred;

The determination of ownership, use rights over the residential house and land parcels is based on the certificate of ownership, land use rights. The individual transferring the house, land is responsible for declaring and ensuring the accuracy of their declaration in accordance with the law. If regulatory agencies find incorrect declarations, tax exemption shall not apply, and penalties shall be imposed as per applicable laws.

3. Income from the value of land use rights of individuals allocated land without land use fee or reduced land levy by the state according to legal provisions.

4. Income from receiving inheritance, gifts in the form of real estate (including residential houses, buildings to be formed as per future real estate business law) between: husband and wife; biological parents and children; adoptive parents and adopted children; parents-in-law and daughter-in-law; parents-in-law and son-in-law; paternal grandparents and grandchildren; maternal grandparents and grandchildren; siblings.*

Therefore, it can be observed that income from the transfer, inheritance, and gifts of movable assets such as money, gold, and valuable documents that do not require ownership registration are not subject to personal income tax.

Is inheritance in the form of money and gold subject to personal income tax in Vietnam? (Image from the Internet)

What are the personal income tax periods for taxable income from inheritance in Vietnam?

According to Article 7 of the 2007 Law on Personal Income Tax (amended by Clause 3, Article 1 of the 2012 Revised Law on Personal Income Tax) outlines the tax period as follows:

Tax Period

1. The tax period for resident individuals is stipulated as follows:

a) The annual tax period applies to income from business; income from wages, salaries;

b) A tax period for each time the income arises applies to income from capital investment; income from capital transfer, except for income from securities transfer; income from real estate transfer; income from winnings; income from royalties; income from franchising; income from inheritance; income from gifts;*

c) A tax period for each transfer or annually for income from securities transfer.

2. The tax period for non-resident individuals is calculated for each time the income arises for all taxable income.

Therefore, according to the above provisions, the personal income tax for income from inheritance follows a tax period for each occurrence of income generation.

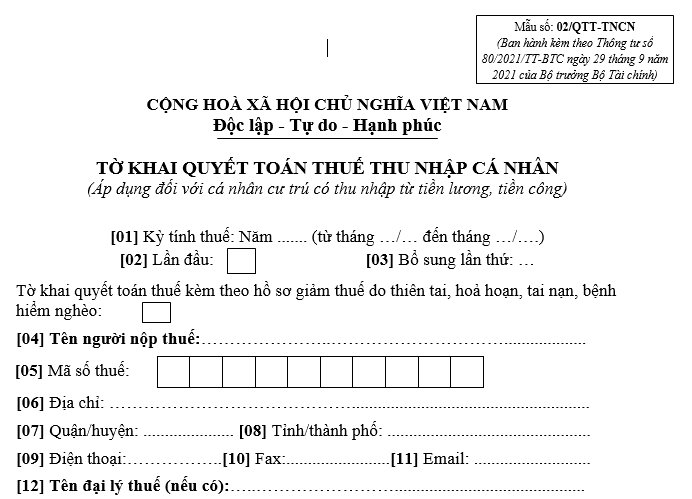

What is the form for the personal income tax settlement declaration in Vietnam?

The form for the personal income tax settlement declaration applicable to individuals with income from wages and salaries is form 02/QTT-TNCN, issued together with Circular 80/2021/TT-BTC, specifically:

>>> Download the form for the personal income tax settlement declaration applicable to individuals with income from wages and salaries