How to look up fixed tax payer information on the General Department of Taxation of Vietnam?

How to look up fixed tax payer information on the General Department of Taxation of Vietnam?

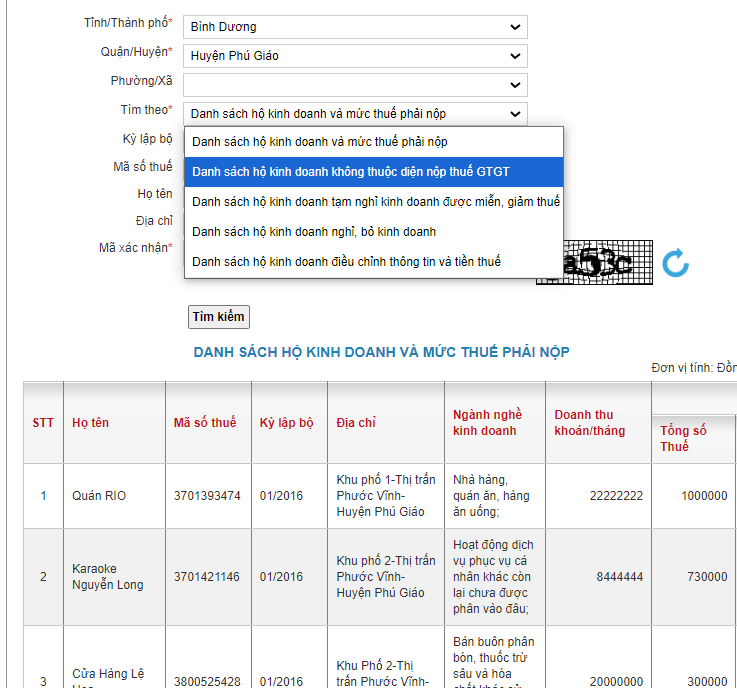

Taxpayers can check fixed tax payer information on the General Department of Taxation of Vietnam by following these instructions:

Step 1: Access https://www.gdt.gov.vn/wps/portal and scroll to the bottom of the General Department of Taxation of Vietnam's homepage.

Step 2: Taxpayers enter the following information:

- Province, city, district, more specifically can search by Ward/Commune

- Search by: List of household businesses and payable tax amount, List of household businesses not paying VAT...

- Enter the verification code.

Step 3: The result list displays.

How to look up fixed tax payer information on the General Department of Taxation of Vietnam?

When is the deadline for submitting fixed tax declaration in Vietnam?

Based on Clause 3, Article 13 of Circular 40/2021/TT-BTC, the deadline for submitting fixed tax declaration is regulated as follows:

Tax management for household businesses

...

3. Deadline for submitting tax declaration

The deadline for submitting tax declaration for household businesses is specified in point c, clause 2, clause 3 of Article 44 of the Law on Tax Administration. Specifically:

a) The deadline for submitting tax declaration for household businesses is no later than December 15 of the year preceding the tax calculation year.

b) In case of new business start-up households (including those switching to the presumptive method), households switching to the declaration method, households changing business sectors, or households changing business scales during the year, the deadline for submitting tax declaration is no later than the 10th day from the start of business, method change, business sector change, or business scale change.

c) The deadline for submitting tax declaration for household businesses using invoices issued by the tax authority, retailed per transaction, is no later than the 10th day from the date of revenue occurrence with invoice usage requests.

What are regulations on tax calculation methods for household businesses and individual businesses paying fixed tax in Vietnam?

Pursuant to Article 7 of Circular 40/2021/TT-BTC as amended by Clause 1, Article 1 of Circular 100/2021/TT-BTC.

- The presumptive method applies to household businesses and individual businesses not required to pay taxes through the declaration method and not required to pay taxes per transaction as guided in Articles 5 and 6 of Circular 40/2021/TT-BTC.

- Household businesses and individual businesses paying fixed tax (fixed tax payers) are not required to implement accounting policies. fixed tax payers using singular invoices must store and present to tax authorities invoices, documents, contracts, and files proving the legitimacy of goods and services when requesting invoice issuance on a per-transaction basis.

In particular, fixed tax payers doing business in border markets, border-gate markets, and markets within border-gate economic zones in Vietnam must store invoices, documents, contracts, files proving legitimate goods, and present them when requested by competent state management authorities.

- Fixed tax payers that have been notified by the tax authority of the tax amount due from the beginning of the year must pay taxes as instructed. If a fixed tax payer that was notified of the tax amount from the beginning of the year stops or temporarily suspends business within the year, the tax authority will adjust the tax amount due as guided at point b.4, point b.5, clause 4, Article 13 of Circular 40/2021/TT-BTC.

If a new fixed tax payer starts business within the year (not a full 12 months in the calendar year), the household is required to pay VAT and personal income tax (PIT) if the annual business revenue exceeds 100 million VND; or not required to pay VAT or PIT if the annual business revenue is 100 million VND or less.

- Fixed tax payers declare taxes annually as stipulated in point c, clause 2, Article 44 of the Law on Tax Administration, and pay taxes by the deadline specified in the tax authority's Notice of Tax Payment as regulated in clause 2, Article 55 of the Law on Tax Administration.

If a fixed tax payer uses invoices issued by the tax authority, retails per number, the household must declare and pay taxes separately for the revenues on that invoice per transaction occurrence.