How to declare taxes for individuals leasing assets who directly declare taxes with the tax authority in Vietnam?

How to declare taxes for individuals leasing assets who directly declare taxes with the tax authority in Vietnam?

Based on Subsection 112, Section II of the administrative procedures issued with Decision 1462/QD-BTC of 2022, the guideline for tax declaration for individuals leasing property who directly declare taxes to the tax authority is as follows:

Step 1.

- Individuals with leased assets prepare their tax declaration dossier for each instance or annually.

- Deadline for submitting the tax declaration dossier: no later than the last day of the first month of the calendar year or fiscal year if the individual opts to declare taxes once a year; or no later than the 10th day from the start of the lease term of the payment period if the individual declares taxes each occurrence of payment.

- Place for submitting the tax declaration dossier: Individuals earning income from leasing assets (except real estate in Vietnam) submit the tax declaration dossier at the tax authority where the individual resides. Individuals earning income from leasing real estate in Vietnam submit the tax declaration dossier at the tax authority where the real estate is located.

Step 2. The tax authority receives the taxpayer's dossier:

- In cases where the dossier is submitted directly at the tax authority or sent via postal service: the tax authority processes and handles the dossier as per regulations.

- In cases where the dossier is submitted to the tax authority via electronic transactions, the receipt, inspection, acceptance, and resolution of the dossier (and results if applicable) are conducted through the electronic data processing system of the tax authority.

Regarding the method of execution:

- Submit directly at the tax authority office;

- Or send via the postal system;

- Or submit the electronic dossier to the tax authority via electronic transactions (The General Department of Taxation's electronic portal/the electronic portal of the competent state agency or T-VAN service provider organization).

How to declare taxes for individuals leasing assets who directly declare taxes with the tax authority in Vietnam? (Image from the Internet)

What is the tax declaration dossier for individuals leasing assets who directly declare taxes with the tax authority in Vietnam?

Based on Subsection 112, Section II of the administrative procedures issued with Decision 1462/QD-BTC of 2022 and Clause 1, Article 14 Circular 40/2021/TT-BTC, the tax declaration dossier for individuals leasing property who directly declare taxes with the tax authority includes:

- Tax declaration for asset leasing activities (applicable for individuals undertaking asset leasing activities directly declaring taxes with the tax authority and organizations declaring on behalf of individuals) form 01/TTS according to Appendix I - List of tax declaration dossiers issued with Decree 126/2020/ND-CP and Appendix II - List of forms issued with Circular 40/2021/TT-BTC.

- Appendix of a detailed list of asset leasing contracts (applicable for individuals undertaking asset leasing activities directly declaring taxes with the tax authority if it is the first tax declaration of the Contract or the Contract Appendix) form 01-1/BK-TTS according to Appendix I - List of tax declaration dossiers issued with Decree 126/2020/ND-CP and Appendix II - List of forms issued with Circular 40/2021/TT-BTC;

- Copy of the asset lease contract, contract appendix (if it is the first tax declaration of the Contract or Contract Appendix);

- Copy of the Power of Attorney as stipulated by law (in case the individual leasing the property authorizes a legal representative to carry out tax declaration and payment procedures).

The tax authority has the right to request verification of the original documents to confirm the accuracy of the copies compared to the original documents.

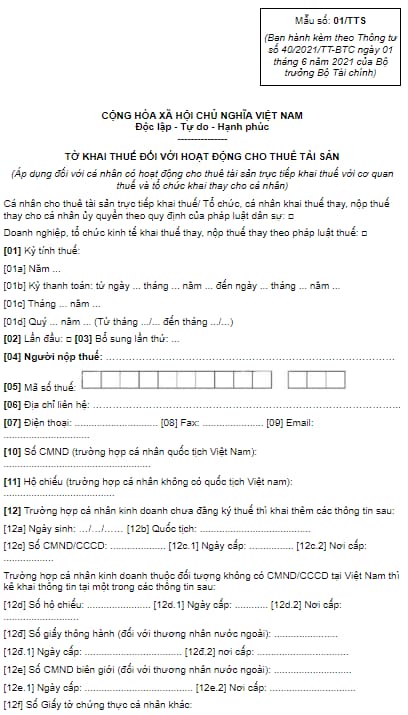

What is the tax declaration form for individuals leasing assets who directly declare with the tax authority in Vietnam?

Based on Form 01/TTS Appendix II issued with Circular 40/2021/TT-BTC, the tax declaration form is specified as follows:

Download form 01/TTS here: download

Where is the location for directly submitting the tax declaration dossier for asset leasing for individuals in Vietnam?

Based on Clause 2, Article 14 of Circular 40/2021/TT-BTC the provision is as follows:

The place to submit the tax declaration dossier for individuals leasing assets who directly declare taxes with the tax authority as specified in Clause 1, Article 45 of the Law on Tax Administration. Specifically:

- Individuals earning income from leasing assets (except real estate in Vietnam) submit the tax declaration dossier at the Tax Department that directly manages where the individual resides.

- Individuals earning income from leasing real estate in Vietnam submit the tax declaration dossier at the Tax Department that directly manages where the real estate is leased.