How to calculate profit before tax on the income statement in Vietnam?

How to calculate profit before tax on the income statement in Vietnam?

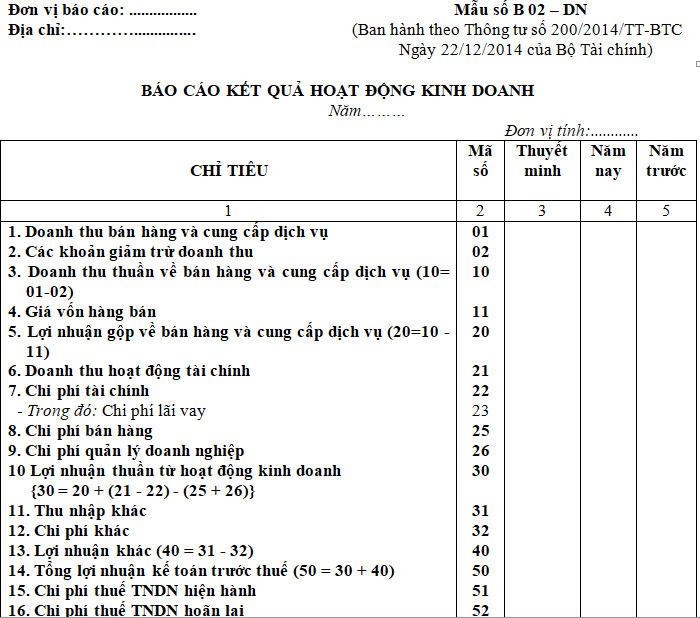

Profit before tax is indicated as entry 50 on the income statement according to Form No. B02-DN, issued together with Circular 200/2014/TT-BTC.

To be specific, in point 3.15, clause 3, Article 113 of Circular 200/2014/TT-BTC:

Guidelines for Preparing and Presenting the income statement (Form No. B02-DN)

...

3. Content and Method for Preparing the Indicators in the income statement

...

3.15. Total Accounting Profit Before Tax (Code 50):

This indicator reflects the total accounting profit realized in the reporting year of the enterprise before deducting corporate income tax expenses from business activities and other activities arising during the reporting period. Code 50 = Code 30 + Code 40.

Profit before tax reflects the total accounting profit realized in the reporting year of the enterprise before deducting corporate income tax expenses from business activities and other activities arising during the reporting period.

Profit before tax includes all gains from production and business activities, financial profit, and other resulting profits. Profit before tax is calculated as total revenue minus expenses.

The formula to calculate profit before tax is as follows:

| Total Profit Before Tax = Net Profit from Business Activities + (Other Income - Other Expenses) |

How to calculate profit before tax on the income statement in Vietnam? (Image from the Internet)

What is the Form B02-DN on income statement in Vietnam?

Currently, the income statement uses Form No. B02-DN issued together with Circular 200/2014/TT-BTC, structured as follows:

Download the income statement form here: Download

Vietnam: What does the content and structure of the report include?

Based on clause 1, Article 113 of Circular 200/2014/TT-BTC, the provisions are as follows:

Guidelines for Preparing and Presenting the income statement (Form No. B02-DN)

1. Content and structure of the report:

a) The income statement reflects the situation and results of business activities of the enterprise, including the results from the main business activities and the results from financial activities and other activities of the enterprise.

When preparing the consolidated income statement between the enterprise and its lower-level units without legal status and dependent accounting, the enterprise must eliminate all revenue, income, and expense items arising from internal transactions.

b) The income statement consists of 5 columns:

- Column 1: Reporting indicators;

- Column 2: Code for the corresponding indicators;

- Column 3: Corresponding numbers for the indicators of this report as displayed in the Notes to Financial Statements;

- Column 4: Total occurrence during the reporting year;

- Column 5: Figures of the previous year (for comparison).

2. Basis for preparing the report

- Based on the income statement of the previous year.

- Based on the general and detailed bookkeeping records for the period used for accounts from type 5 to type 9.

The income statement reflects the situation and results of business activities of the enterprise, including the results from the main business activities and the results from financial activities and other activities of the enterprise.

When preparing the consolidated income statement between the enterprise and its subordinate units without legal status and dependent accounting, the enterprise must eliminate all revenue, income, and expense items arising from internal transactions.

The income statement consists of 5 columns:

- Column 1: Reporting indicators;

- Column 2: Code for the corresponding indicators;

- Column 3: Corresponding numbers for the indicators of this report as displayed in the Notes to Financial Statements;

- Column 4: Total occurrence during the reporting year;

- Column 5: Figures of the previous year (for comparison).