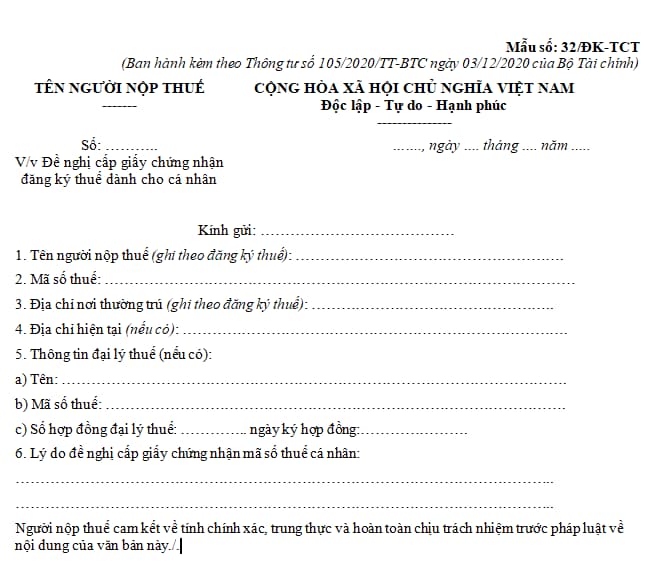

Form No. 32/DK-TCT: What is the Application for issuance of certificate of tax registration for individuals in Vietnam?

Form No. 32/DK-TCT: What is the Application for issuance of certificate of tax registration for individuals in Vietnam?

The document requesting the issuance of the certificate of tax registration for individuals using form No. 32/DK-TCT is issued in accordance with Circular 105/2020/TT-BTC as follows:

>> Download the document requesting the issuance of the certificate of tax registration for individuals using form No. 32/DK-TCT

Form No. 32/DK-TCT: What is the Application for issuance of certificate of tax registration for individuals in Vietnam? (Image from the Internet)

What information is included in the certificate of tax registration in Vietnam?

Based on Article 34 of the Tax Administration Law 2019 regarding the issuance of certificate of tax registrations as follows:

Issuance of certificate of tax registrations

1. The tax authority shall issue a certificate of tax registration to the taxpayer within 3 business days from the date of receipt of the complete taxpayer registration dossier as prescribed. The information on the certificate of tax registration includes:

a) Name of the taxpayer;

b) Tax code;

c) Number, date, month, and year of the business registration certificate or establishment and operational license or investment registration certificate for business organizations and individuals; number, date, month, and year of the establishment decision for organizations not required to register for business; information from the identity card, citizen identification card, or passport for individuals not required to register for business;

d) Directly managing tax authority.

2. The tax authority will notify the taxpayer of their tax code instead of issuing a certificate of tax registration in the following cases:

a) Individuals authorizing organizations or individuals to pay income on their behalf and register for taxpayers and their dependents;

b) Individuals registering for taxpayers through tax declaration dossiers;

c) Organizations or individuals registering for taxpayers to deduct tax and pay on behalf of individuals;

d) Individuals registering for taxpayers for their dependents.

...

Thus, the certificate of tax registration includes the following information:

- Name of the taxpayer;

- Tax code;

- Number, date, month, and year of the business registration certificate or establishment and operational license or investment registration certificate for business organizations and individuals; number, date, month, and year of the establishment decision for organizations not required to register for business; information from the identity card, citizen identification card, or passport for individuals not required to register for business;

- Directly managing tax authority.

What is the time limit for issuance of certificate of tax registration of the tax authority in Vietnam?

Based on Clause 1, Article 34 of the Tax Administration Law 2019, the tax authority must issue the certificate of tax registration to the taxpayer within 3 business days from the date of receipt of the complete taxpayer registration dossier as prescribed.

What is the procedure for reissuing a damaged certificate of tax registration in Vietnam?

Based on Subsection 18, Section 1, Part 2 Procedures issued with Decision 2589/QD-BTC 2021, the first-time registration procedure for dependents directly at the tax authority is detailed as follows:

Step 1.

- Taxpayers who have lost, torn, or burned their certificate of tax registration or the Tax Registration Notification for dependents should submit a dossier for reissuing the certificate of tax registration or Tax Registration Notification to the directly managing tax authority.

- For electronic registration dossiers: Taxpayers (NNT) access the electronic portal of their choice to fill out the declaration form and attach the prescribed documents in electronic form (if any), electronically sign and send to the tax authority via the selected electronic portal.

Taxpayers submit the dossiers (registration dossiers together with business registration dossiers according to the one-stop inter-connected mechanism) to the competent state management agency as prescribed. The competent state management agency sends the received dossier information of the taxpayer to the tax authority via the General Department of Taxation's electronic portal.

Step 2. Tax Authority's Reception:

- For paper registration dossiers:

+ In case the dossier is submitted directly at the tax authority: Tax officers receive and stamp the dossier of taxpayer registration, indicating the date of receipt, the number of documents according to the checklist for dossiers submitted directly at the tax authority. Tax officers issue a receipt stating the date of return and processing time for the accepted dossier.

+ In case the registration dossier is sent via postal service: Tax officers stamp the receipt, indicating the date of receipt and record the number of the tax authority’s dispatch.

Tax officers check the registration dossier. If the dossier is incomplete and requires clarification or additional information, the tax authority will notify the taxpayer using form No. 01/TB-BSTT-NNT within 2 business days from the date of receipt of the dossier.

- For electronic registration dossiers:

The tax authority receives the dossier via the electronic portal of the General Department of Taxation, checks, and processes the dossier through the tax authority's electronic data processing system:

+ Receipt of the dossier: The General Department of Taxation's electronic portal sends a receipt notification to the taxpayer via the electronic portal chosen by the taxpayer to submit the dossier (the General Department of Taxation's electronic portal/state authority’s electronic portal or the T-VAN service provider’s electronic portal), no later than 15 minutes from the receipt of the taxpayer's electronic registration dossier.

+ Dossier review and processing: The tax authority checks and processes the taxpayer's dossier according to the legal regulations on taxpayer registration and delivers the results via the chosen electronic portal:

++ If the dossier is complete and correct according to regulations and results need to be provided: The tax authority sends the dossier processing result to the selected electronic portal chosen by the taxpayer for submitting the dossier within the stipulated time.

++ If the dossier is incomplete and does not meet the regulatory procedure requirements, the tax authority sends a notification of rejection to the chosen electronic portal within 2 business days from the date on the receipt notification.