Are investors of multiple investment projects in Vietnam exempt from non-agricultural land use tax for all investment projects?

Are investors of multiple investment projects in Vietnam exempt from non-agricultural land use tax for all investment projects?

Based on Article 11 of the 2010 Law on Non-agricultural Land Use Tax:

Principles of tax exemption and reduction

1. Taxpayers entitled to both tax exemptions and reductions for the same parcel are granted an exemption; taxpayers eligible for multiple tax reductions under Article 10 of this Law are granted an exemption.

2. Taxpayers on homestead land are only eligible for tax exemptions or reductions at one location of their choice, except in cases specified in Clause 9, Article 9 and Clause 4, Article 10 of this Law.

3. Taxpayers with multiple investment projects eligible for tax exemptions or reductions will be granted such exemptions or reductions for each individual investment project.

4. Tax exemptions and reductions only apply directly to the taxpayer and only count towards the amount of tax payable as prescribed by this Law.

Thus, in the case where all investment projects of an investor fall under the non-agricultural land use tax exemption category, the investor will be exempt from tax for all investment projects.

Are investors of multiple investment projects in Vietnam exempt from non-agricultural land use tax for all investment projects? (Image from the Internet)

What types of land are eligible for non-agricultural land use tax exemption in Vietnam?

Based on Article 9 of the 2010 Law on Non-agricultural Land Use Tax, the cases eligible for non-agricultural land use tax exemption include:

- Land for investment projects in specially encouraged investment sectors; investment projects in areas with particularly difficult socio-economic conditions; investment projects in encouraged investment sectors in areas with difficult socio-economic conditions; land of enterprises employing more than 50% of the workforce being war invalids and sick soldiers.

- Land of facilities undertaking private investment in activities in the fields of education, vocational training, health care, culture, sports, and the environment.

- Land used for constructing gratitude houses, great solidarity houses, facilities for nurturing lonely elderly, disabled people, orphans; social rehabilitation facilities.

- Residential land within the limit in areas with particularly difficult socio-economic conditions.

- Residential land within the limit of individuals who were active in the revolution before August 19, 1945; war invalids of ranks 1/4 and 2/4; individuals entitled to policies as war invalids of ranks 1/4 and 2/4; sick soldiers of rank 1/3; heroes of the people’s armed forces; Vietnamese Heroic Mothers; biological parents, individuals who fostered martyrs as children; spouses of martyrs; children of martyrs receiving monthly allowances; individuals active in the revolution affected by Agent Orange; individuals affected by Agent Orange with difficult family circumstances.

- Residential land within the limit of households classified as poor as per the regulations of the Government of Vietnam.

- Households and individuals having their homestead land expropriated in a year as per plans approved by competent state authorities will be exempt from tax in the year of actual land expropriation for land at the expropriated location and the new place of residence.

- Land with garden houses recognized by competent state authorities as historical-cultural relics.

- Taxpayers facing difficulties due to force majeure events, if the value of damage to land and houses on the land exceeds 50% of the taxable value.

Who is not subject to non-agricultural land use tax in Vietnam?

Based on Article 3 of the 2010 Law on Non-agricultural Land Use Tax, the following entities are not subject to non-agricultural land use tax:

- Land used for public purposes including roads, irrigation; land for constructing public cultural, health care, education and training, and sporting facilities; land with historical-cultural relics and scenic spots; land used for constructing other public works as per the regulations of the Government of Vietnam;

- Land used by religious organizations;

- Land used for cemeteries;

- Rivers, canals, streams, and specialized water surfaces;

- Land with structures such as temples, shrines, worship houses, family ancestral halls, and family places of worship;

- Land used for constructing agency headquarters, undertaking official business, land used for national defense and security purposes;

- Other non-agricultural land as stipulated by law.

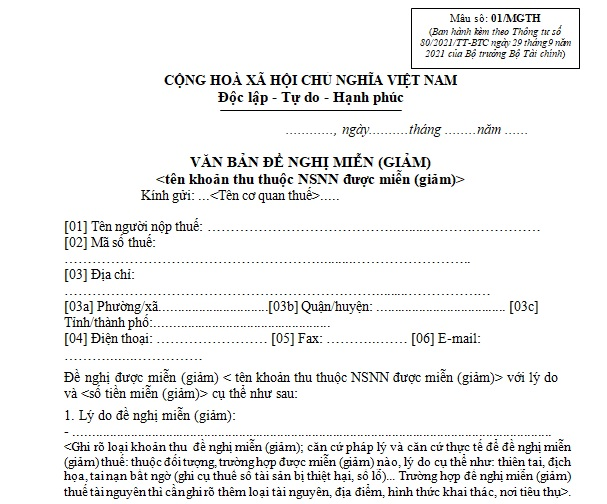

What is the Form for requesting non-agricultural land use tax exemption or reduction in Vietnam?

The Form for requesting non-agricultural land use tax exemption or reduction in Vietnam is form 01/MGTH issued alongside Appendix 1 of Circular 80/2021/TT-BTC:

Download Form 01/MGTH - Form for requesting non-agricultural land use tax exemption or reduction: Here