Tet bonus, 13th month salary is always an issue that employees and businesses care about when there is only 1 month left to enter 2021. LAWNET would like to send to Customers and Members the latest Tet bonus decision form applied from 2021 in Vietnam.

Article table of contents

Article table of contents

According to Article 104 of the Labor Code 2019 of Vietnam (officially effective from January 01, 2021), a bonus means an amount of money, a piece of property or item that is provided by an employer for his/her employees on the basis of the business performance or the employees’ performance.

Concurrently, a bonus regulation shall be decided and publicly announced at the workplace by the employer after consultation with the representative organization of employees (if any).

Thus, according to the above provisions, from January 01, 2021, enterprises giving Tet bonuses to employees will not necessarily have to pay in cash (as prescribed in the Labor Code 2012 of Vietnam) but can be more flexible in forms such as cash; with products and services available in the enterprise or real assets with the needs of employees; or by other means. However, regardless of the form of Tet bonus in 2021, enterprises still need to publicly announce the bonus policy at work after consulting with the representative organization of employees (if any).

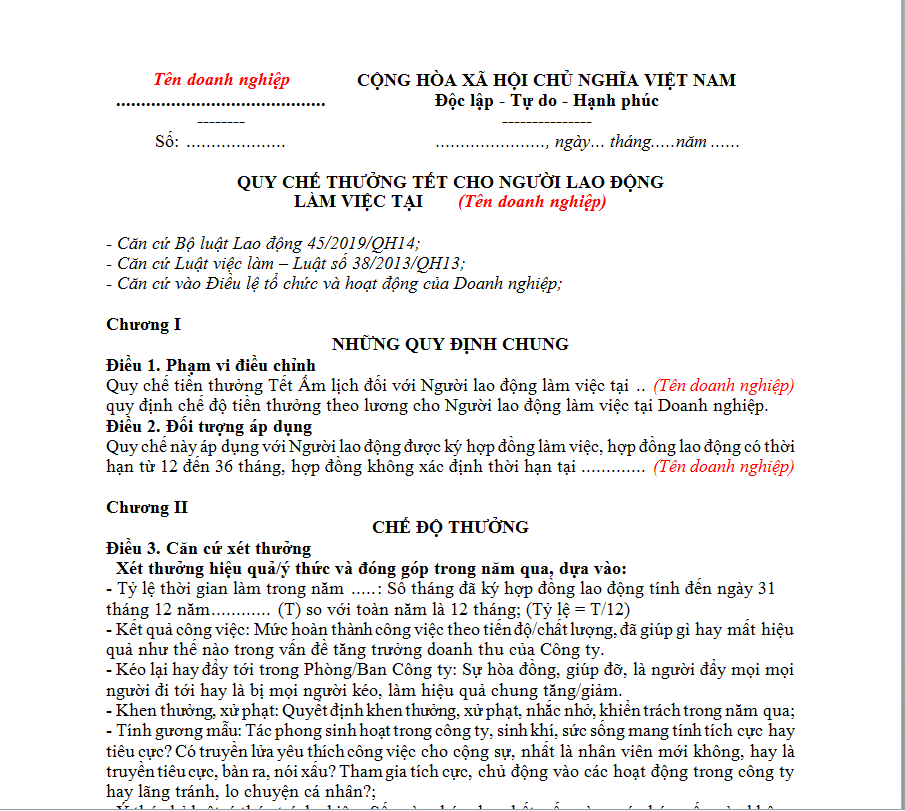

Accordingly, in order to save time in drafting the Regulation on Tet bonus in 2021 for employees, LAWNET would like to send to Customers and Members the latest form of the New Year bonus from 2021 as follows:

DOWNLOAD: Latest form of Regulation on Tet bonus from 2021 in Vietnam

Note: The bonus regulation is decided by the enterprise and publicly announced at the workplace after consulting with the representative organization of the labor collective at the grassroots level. Concurrently, the promulgation of the Regulation on Tet bonus and reward must stipulate the subjects and conditions for receiving the bonus, the calculation method, and the reward level. Because this is the basis, the conditions for the bonus payment can be considered as a reasonable expense when determining the taxable income of the enterprise.

Ty Na

- Key word:

- Labor Code 2019

- Tet bonus

.Medium.png)

.Medium.png)

.Medium.png)

.Medium.png)