Vietnam: How much salary is required for teachers to pay personal income tax (PIT)?

How much salary must a teacher earn to pay personal income tax?

Pursuant to the taxable income items specified in Article 2 of Circular 111/2013/TT-BTC of the Ministry of Finance of Vietnam:

Taxable income items

…

2. Income from wages and salaries

Income from wages and salaries is the income received by employees from employers, including:

a) Wages, salaries, and similar items in the form of money or non-money.

b) Allowances and subsidies, except for the following allowances and subsidies:

b.1) Monthly preferential subsidies and one-time subsidies as per the regulations concerning the preferential treatment of individuals with meritorious services.

…

In addition, based on Article 1 of Resolution 954/2020/UBTVQH14, the family deduction levels are specified as follows:

Family deduction levels

Adjust the family deduction levels stipulated in Clause 1, Article 19 of the Personal Income Tax Law No. 04/2007/QH12, amended and supplemented by Law No. 26/2012/QH13, as follows:

1. The deduction rate for taxpayers is 11 million VND/month (132 million VND/year);

2. The deduction rate for each dependent is 4.4 million VND/month.

Thus, teachers earning income from wages and salaries in Vietnam will be obligated to pay personal income tax as regulated.

Specifically, a teacher without dependents must pay personal income tax if the total income from wages and salaries exceeds 11 million VND/month (this income has already deducted mandatory insurance contributions and charitable, humanitarian donations...), if the teacher registers a family deduction for one dependent, then it exceeds 15.4 million VND.

How much salary must a teacher earn to pay personal income tax? (Image from the Internet)

How to calculate the salary of teachers who are public employees from July 1, 2024?

According to Circular 07/2024/TT-BNV of the Ministry of Home Affairs of Vietnam, the salary of teachers who are public employees is calculated as follows:

Salary = Basic salary x Salary coefficient

Additionally, when increasing the statutory base rate to 2,340,000 VND/month, the teacher's salary is calculated as follows:

Salary = 2,340,000 VND x Salary coefficient

*Unit: VND/month

Note: The above-mentioned salary does not include allowances and support that officials and public employees receive.

How is the personal income tax calculated for teachers with sufficient salary income?

Below is the personal income tax calculation for teachers' salaries:

According to the regulations in Article 7, Article 8 of Circular 111/2013/TT-BTC, personal income tax from wages and salaries for resident individuals is determined as follows:

| PIT from wages and salaries = Taxable income from wages and salaries x Tax rate |

In which:

Taxable income = Total taxable income - Deductible expenses

Total taxable income = Total income - Exempted items

Taxable income from wages and salaries is determined by the total income from wages and salaries that the taxpayer receives during the tax period, including:

- Wages, salaries, and similar items;- Allowances and subsidies, excluding:

+ Allowances and subsidies according to preferential policies for individuals with meritorious services;

+ Defense and security allowances;

+ Hazardous and dangerous allowances for jobs or workplaces with hazardous and dangerous factors;

+ Attraction and regional allowances as per the regulations;

+ Unexpected hardship allowances, labor accident allowances, occupational disease allowances, one-time allowances for childbirth or adoption, allowances for reduced working capacity, one-time pension allowances, monthly survivor benefits, and other allowances as stipulated by social insurance laws;

+ Severance allowances, job loss allowances as stipulated in the Labor Code 2019;

+ Social protection allowances and other allowances and subsidies not in the nature of wages or salaries as per the regulations of the Government of Vietnam.

Personal income tax deductions include:

- Social insurance, health insurance, unemployment insurance, professional liability insurance (for certain mandatory insurance sectors), voluntary pension fund contributions;

- Family deductions:

The family deduction levels are currently implemented according to Resolution 954/2020/UBTVQH14, as follows:

- Deduction rate for taxpayers is 11 million VND/month (132 million VND/year);

- Deduction rate for each dependent is 4.4 million VND/month.

- Deductions for charitable, humanitarian donations:

Charitable, humanitarian donations are deducted from income before calculating tax on business income, wages, and salaries of resident taxpayers, including:

- Contributions to organizations and facilities that care for and nurture children in especially difficult circumstances, the disabled, and the elderly without support;

- Contributions to charity, humanitarian funds, and study encouragement funds.

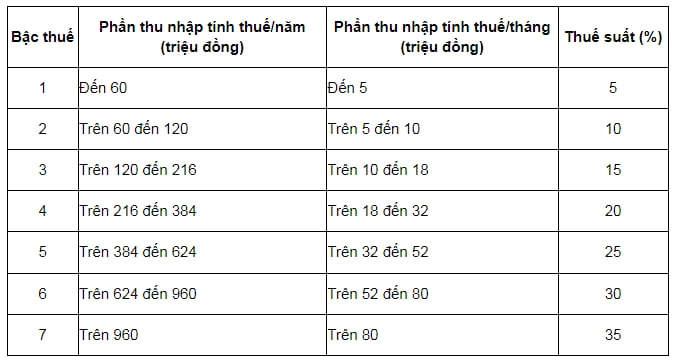

Personal income tax rates:

The progressive tax rate schedule is specified in Clause 2, Article 7 of Circular 111/2013/TT-BTC as follows: