Vietnam: What is the registration form for depreciation of fixed assets at agencies, organizations, units and fixed assets assigned by the State to enterprises for management?

- What is the registration form for depreciation of fixed assets at agencies, organizations, units and fixed assets assigned by the State to enterprises for management in Vietnam?

- What are the regulations on scope of depreciation calculation of fixed assets in Vietnam?

- What are the rules for calculating depreciation of fixed assets in Vietnam?

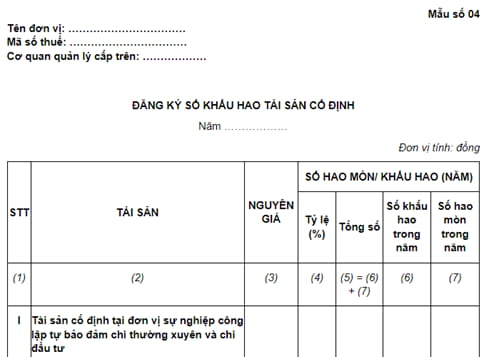

What is the registration form for depreciation of fixed assets at agencies, organizations, units and fixed assets assigned by the State to enterprises for management in Vietnam?

The registration form for depreciation of fixed assets at agencies, organizations, units and fixed assets assigned by the State to enterprises for management is specified in Form No.04, Appendix 2 issued together with Circular 45/2018/TT-BTC as follows:

See the registration form for depreciation of fixed assets: Here.

What are the regulations on scope of depreciation calculation of fixed assets in Vietnam?

Pursuant to Article 12 of Circular 45/2018/TT-BTC stipulating the scope of of depreciation calculation of fixed assets as follows:

- The current fixed assets of agencies, organizations and units and the fixed assets provided to the enterprises by the state without calculation of the state capital portion shall be calculated for their depreciation, except the cases specified in clause 2, clause 3 of this Article.

- The fixed assets of public sector entities must be depreciated according to Article 16 hereof, including:

+ The fixed assets of public sector entities that pay for the regular expenses and investment expenses themselves.

+ The fixed assets of public sector entities which require its depreciation to be included in the service price according to the law.

+ The fixed assets of public sector entities which are not specified in point a and b of this clause shall be used in business activities, leasing activities, joint venture and association activities without establishing new legal entity.

- The following fixed assets shall not be calculated for their depreciation:

+ The fixed assets are the land use rights which must be determined to be included in the value of such assets as specified in Article 100 of the Decree No. 151/2017/ND-CP

+ The special fixed assets specified in Article 5 hereof, except the fixed assets which are brands of public sector entities and are used in joint venture and association activities without establishing new legal entity according to point c, clause 2 of this Article.

+ Rented fixed assets.

+ Fixed assets being kept on behalf of the State.

+ Fixed assets that are still usable after their depreciation is being fully calculated or their costs are being completely depreciated.

+ Fixed assets that are not usable though their depreciation is not fully calculated and their costs are not completely depreciated.

What are the rules for calculating depreciation of fixed assets in Vietnam?

Pursuant to Article 13 of Circular 45/2018/TT-BTC stipulating the the rules for calculating depreciation of fixed assets as follows:

Rules for calculating depreciation of fixed assets and depreciate them

1. Rules for calculating depreciation of fixed assets

a. The depreciation of fixed assets shall be calculated once every year in December before the accounting book is closed. The scope of fixed assets being calculated for their depreciation is for all current fixed assets specified in clause 1, Article 12 hereof, by December 31 of the calculating year.

b. The depreciation of the fixed assets specified in point c, clause 2, Article 12 hereof shall be calculated and such assets shall also be depreciated according to the regulations in Article 16 hereof.

c. If the agencies, organizations, units or enterprises are transferred, split, merged or dissolved, the depreciation of their fixed assets during the financial year, in which the competent agency or the competent person decides such transfer, separation, merging and dissolution, shall be calculated at the receiving agencies, organizations, units or enterprises.

d. If the fixed assets are counted and evaluated according to the decision of the competent agency or the competent person, the depreciation of such assets shall be determined on the basis of revaluation after stocktaking in the financial year in which the competent agency or competent person determines the revaluated value.

2. Rules for depreciating fixed assets

a. The rules for depreciating the fixed assets specified in point a and b, clause 2 and Article 12 hereof shall be applied in accordance with the regulations for enterprises.

b. As for the fixed assets specified in point c, clause 2, Article 12 hereof, the depreciation shall be carried out from the date on which such assets are put into use in the following activities: business, leasing, joint venture and association. The depreciation of such assets shall be stopped after the date on which such assets stop being used for the above activities.

c. The depreciation cost shall be allocated for each professional activity, business activity, leasing activity, joint venture activity and association activity in order to record the cost of each corresponding activity.

Thus, when calculating depreciation of fixed assets, competent individuals and organizations must follow the above-mentioned rules.

LawNet